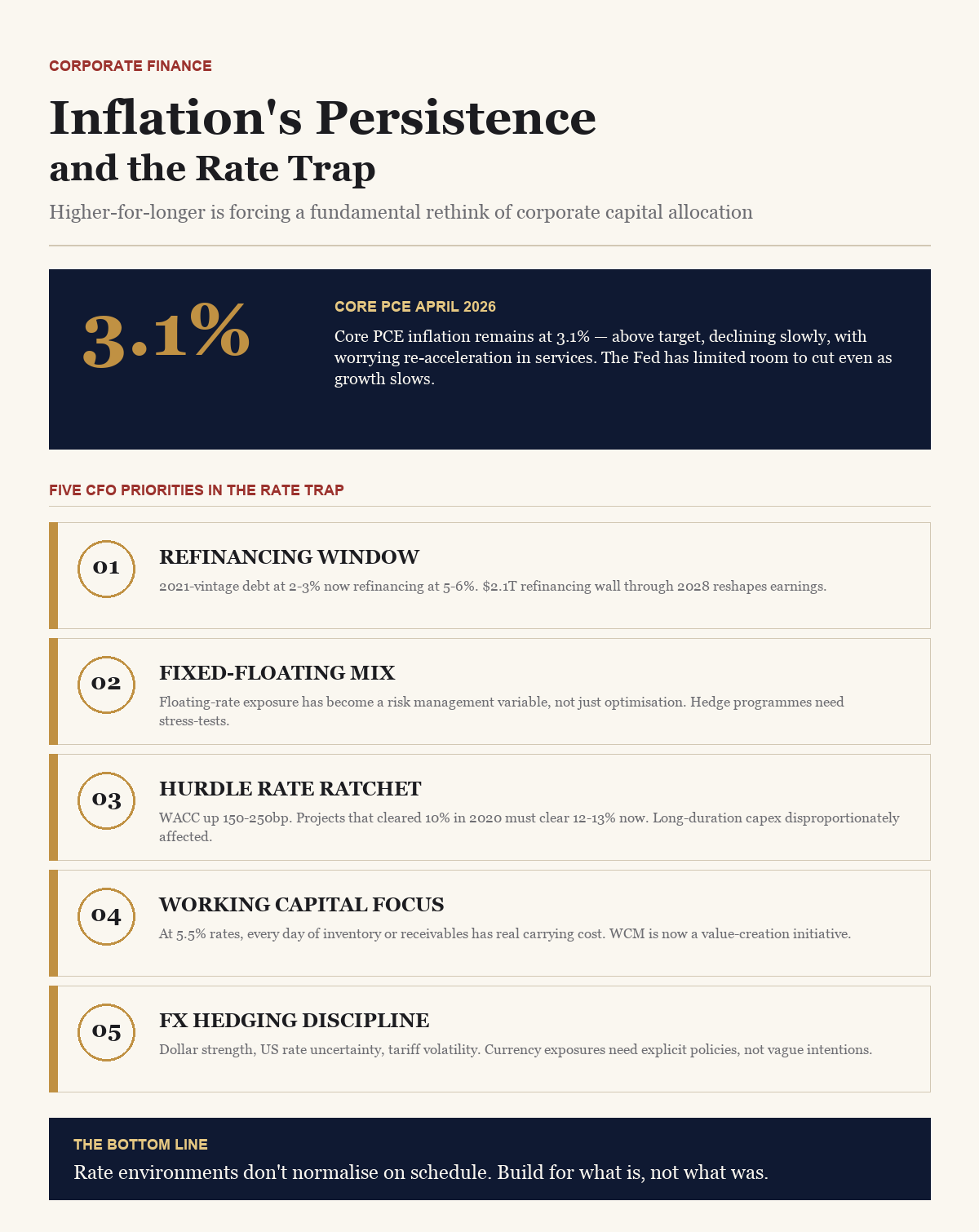

In September 2021, the Federal Reserve‘s median projection for the federal funds rate at the end of 2023 was 0.6%. The actual figure was 5.4%. That 480-basis-point forecast error — the largest in the Fed’s modern projecting history — is a useful calibration for how confidently any institution, however sophisticated, should hold its views on where rates are heading. By April 2026, the federal funds rate stands at 4.5%, having been cut from its 5.5% peak in three cautious 25-basis-point moves over the preceding year. Core PCE inflation, the Fed’s preferred measure, sits at 3.1% — above target, declining slowly, and showing worrying signs of re-acceleration in services components.

For CFOs and corporate treasurers, this is not an abstract macroeconomic puzzle. It is the operational context in which every capital allocation decision is being made. The cost of capital has structurally reset higher than the 2010-2021 era. The rate path is genuinely uncertain. And the traditional playbook — borrow long at low rates, invest in growth, rely on low discount rates to justify long-horizon projects — is no longer reliable. A new framework is required.

Why Inflation Is Stickier Than Expected

Understanding why inflation has persisted longer than consensus expected is prerequisite to building credible capital allocation models. The initial surge — driven by pandemic-era supply disruptions and fiscal stimulus — has largely unwound. What remains is a more structural constellation of pressures that the standard demand-cooling tools of monetary policy are less well-suited to address.

Services inflation is the most persistent component. Shelter costs — which make up approximately 35% of the CPI basket — have remained elevated because the housing supply shortfall that predates the pandemic has not been resolved. Healthcare services, education, and personal care services have seen wage-driven cost increases that are slow to reverse. These are not cyclical pressures that respond rapidly to higher interest rates; they are structural imbalances with their own dynamics.

Goods inflation, having declined sharply from its 2022 peak, has shown signs of re-acceleration in early 2026 — driven primarily by tariff impacts on imported goods. US tariffs on Chinese goods, reimposed and extended under the current administration, have increased the landed cost of categories including electronics, textiles, and household goods. Supply chain nearshoring — the relocation of production from Asia to Mexico, Eastern Europe, and South Asia — adds costs in the near term, even if it reduces geopolitical risk in the long term. The net effect is a goods price floor that is higher than pre-pandemic, complicating the Fed’s path back to 2%.

The Rate Trap: What It Actually Means

The rate trap is a specific scenario in which the Fed faces a dilemma: inflation remains above target, preventing aggressive rate cuts, while economic growth slows to a point where further restriction risks recession. The IMF’s April 2026 World Economic Outlook revised its US growth forecast down to 1.8% for 2026, citing tariff impacts and tightening financial conditions. Simultaneously, core inflation remained above 3%, giving the Fed limited political space for the easing that growth conditions might otherwise warrant.

This trap has a particular corporate finance dimension. Many companies refinanced their debt at very low rates in 2020 and 2021 — five-year and seven-year bonds issued at 2-3% that are now approaching maturity. The refinancing wall for US investment-grade corporates over the 2026-2028 window is estimated by Goldman Sachs at approximately $2.1 trillion. Companies that issued at 2.5% and must now refinance at 5.5% face immediate, material increases in interest expense that flow directly to earnings. For leveraged buyout portfolios — private equity-backed companies that borrowed heavily at floating rates or short maturities — the pressure is more acute.

JP Morgan‘s 2026 High Yield Outlook estimated that approximately 15% of its tracked US high-yield issuers would face interest coverage ratios below 1.5x at current rates — a level that historically correlates with elevated default risk. That is not a systemic crisis, but it is a meaningful headwind for corporate earnings and M&A activity that CFOs in exposed sectors must account for in their own financial modelling.

Rethinking Debt Strategy

The first dimension of the new capital allocation framework is debt book management. Companies that benefited from the 2020-2021 era of ultralow rates need to assess their refinancing exposure with precision: which instruments mature when, at what rate, and what is the realistic refinancing cost at current and projected future rates.

For companies with near-term maturities — debt due in 2026 or 2027 — the decision to refinance now versus wait for rate cuts is a genuine strategic choice with material P&L implications. Refinancing at 5.5% today locks in a known cost. Waiting for cuts that may not arrive on schedule creates rollover risk and revenue uncertainty. Many treasury teams are opting for a partial hedging approach: refinancing a portion of near-term maturities now to lock in the current rate environment, while retaining flexibility on the remainder (see our analysis in The IPO Window Reopens).

The fixed-versus-floating composition of the debt book also deserves explicit policy attention. In an environment where rate direction is genuinely uncertain, the appropriate mix of fixed and floating rate debt is a risk management question, not merely an optimisation question. Treasuries with large floating-rate exposures should be modelling the earnings impact of rate volatility scenarios, not just central cases, and ensuring that their hedging programmes are sized to those scenarios (see our analysis in The Powell Succession Crisis).

Investment Hurdle Rates: The Invisible Ratchet

Perhaps the most consequential — and least visibly discussed — impact of the rate environment on corporate capital allocation is its effect on investment hurdle rates. A hurdle rate is the minimum return a project must generate to justify capital deployment. It is derived from the weighted average cost of capital, which incorporates both the cost of debt and the equity risk premium (see our analysis in Real Estate in a High-Rate World).

As rates have risen, so has the WACC — for most companies, by 150 to 250 basis points relative to the 2019-2021 average. A project that cleared a 10% hurdle rate in 2020 must now clear 12-13% to earn its cost of capital. That ratchet has eliminated the financial case for a significant number of projects that would have been approved three or four years ago. Long-duration investments — infrastructure, R&D with multi-year payback periods, new market entry requiring sustained losses before profitability — are disproportionately affected, because their cash flows are discounted over longer horizons and therefore more sensitive to the discount rate assumption.

The practical consequence is visible in capex trends. US non-residential private investment grew by just 1.2% in real terms in 2025, down from 5.8% in 2023. Technology companies, which had been aggressive investors through the low-rate era, have become more selective. The exception is AI infrastructure — data centres, GPU clusters, and related buildout — where competitive pressure overrides normal hurdle rate discipline. But outside of AI, the capex cycle has clearly moderated in response to higher cost of capital.

Working Capital as a Strategic Lever

In a high-rate environment, working capital management becomes a direct contributor to shareholder value in ways that are often underestimated. Every pound or rupee tied up in inventory, receivables, or prepayments is capital on which the company is implicitly paying the prevailing financing rate. At 2% interest rates, the cost of carrying excess inventory for 60 days versus 30 days is trivial. At 5.5%, it is material.

Best-in-class CFOs have responded by deploying working capital improvement programmes as a priority capital allocation initiative — not as a cost-reduction exercise but as a capital efficiency exercise with direct free cash flow impact. Accounts receivable days, inventory days, and supplier payment terms are being reviewed with the same analytical rigour previously reserved for acquisition targets or capital projects. Dynamic discounting programmes — allowing suppliers to receive early payment in exchange for a discount — have become popular as a tool for improving supplier financial health while generating risk-free returns on corporate cash.

The India CFO’s Specific Context

Indian CFOs face a rate environment that is distinct from, but interrelated with, the US picture. The Reserve Bank of India has been cautiously easing through 2025 and into 2026, reducing the repo rate to 6.0% from a peak of 6.5% as domestic inflation moderated. But external factors — particularly rupee depreciation risk driven by dollar strength and US tariff uncertainty — have constrained the pace of easing. Indian borrowers with US dollar debt face the compound pressure of high dollar rates and currency volatility.

For Indian manufacturing companies exposed to US tariffs — textiles, chemicals, electronics components — the pricing environment requires renegotiating both revenue assumptions and cost structures simultaneously. Capital allocation decisions that made sense when the rupee was at 82 to the dollar look different at 85 or 87. Treasury teams that have not built explicit currency scenarios into their investment models are flying partially blind in the current environment.

Building Resilience Into the Capital Framework

The broader lesson of the 2021-2026 rate cycle is that capital allocation frameworks built on point-estimate rate forecasts are inadequate for the current environment. The confidence intervals around any honest rate projection are wide enough to encompass scenarios ranging from 3% rates to 6% rates over a three-year horizon. Capital allocation frameworks that are rate-robust — that generate acceptable returns across a wide range of rate scenarios, not just the central case — are more valuable than those optimised for a single forecast.

This means building genuine optionality into capital deployment: phased investments that can be accelerated or deferred as conditions evolve, rather than large upfront commitments that lock in assumptions. It means maintaining balance sheet flexibility — lower leverage, longer duration, more liquidity — that allows the company to act opportunistically when conditions shift rather than being constrained by refinancing pressure at the worst moment. And it means having the analytical capability to revise the capital plan rapidly when the macroeconomic inputs change, rather than treating the annual budget as a fixed document.

The rate trap is real, but it is also navigable. Companies that are clear-eyed about their financing exposures, rigorous about their hurdle rates, and disciplined about working capital will be better positioned than those that are waiting for rates to return to the levels that defined the previous decade. Those levels, on any honest assessment of the structural forces now in play, are not coming back soon.