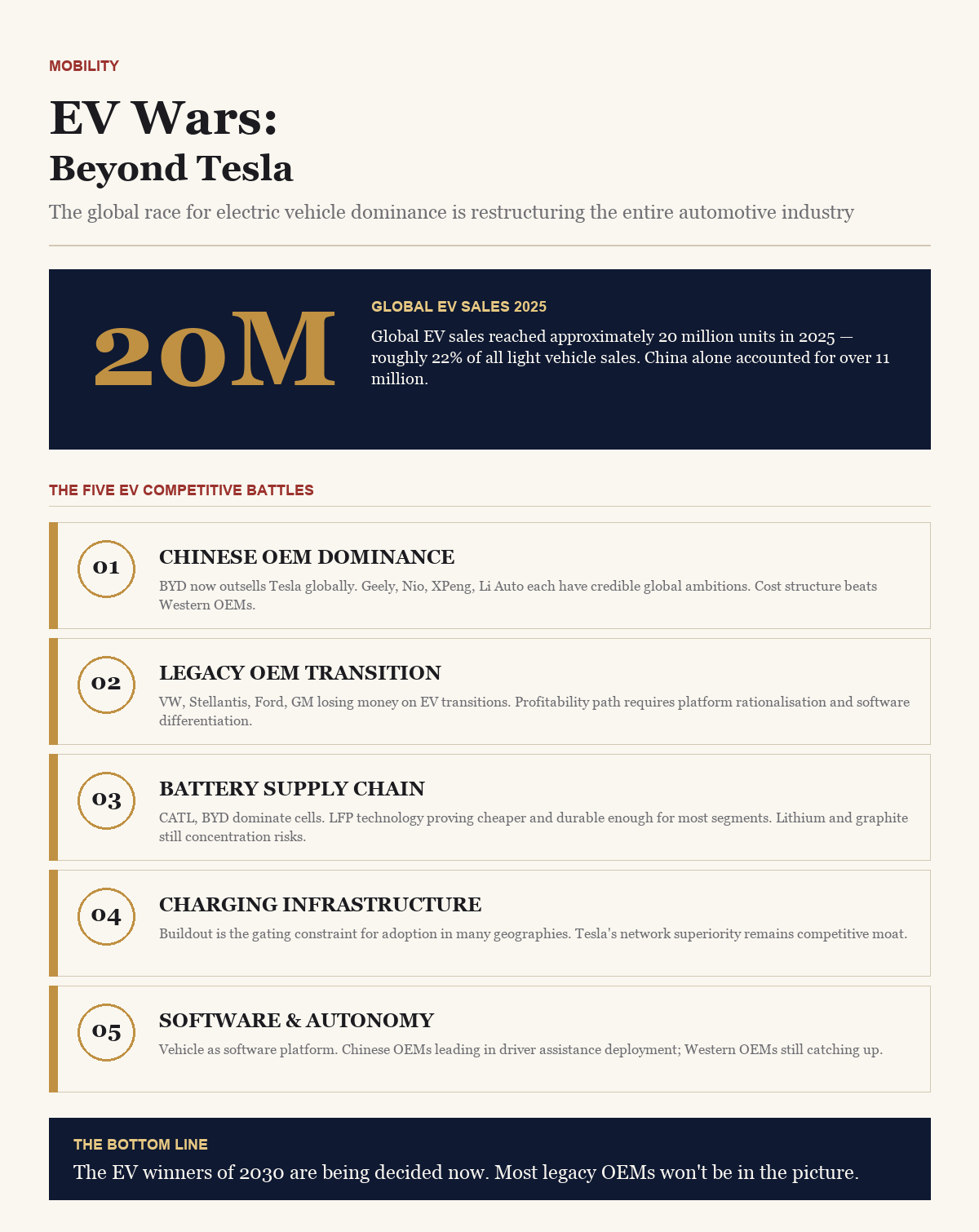

For most of the past decade, Tesla occupied an unusual market position. In a global automotive industry valued at over $3 trillion annually, a single relatively young company commanded approximately 70 per cent of the US electric vehicle market and produced the most influential vehicles in the category. The company’s market valuation peaked above $1 trillion, exceeding the combined market value of every other major automotive manufacturer. The Tesla-as-EV-monopoly era is over. Tesla’s US market share in electric vehicles has declined to approximately 47 per cent in early 2026 and continues to compress. Globally, the company faces serious competitors with credible products, production capacity at scale, and capital resources sufficient to sustain competition through extended periods of margin pressure.

The shift from a Tesla-dominated EV market to a genuinely competitive global market is one of the more consequential industry transitions of the 2020s. Its implications extend beyond the automotive sector to the broader supply chains that support electric vehicles — battery materials, semiconductor components, charging infrastructure, and energy grid services. Understanding the dynamics of this expanded competition is now essential for anyone with exposure to the automotive industry or to the parallel industries that the EV transition is reshaping.

The Chinese EV Industry

The Chinese automotive industry has emerged as the most consequential challenge to Western electric vehicle leadership. BYD, the world’s largest EV manufacturer by volume, produced approximately 4 million electric and plug-in hybrid vehicles in 2025. Geely, NIO, Xpeng, Li Auto, and a growing roster of additional Chinese manufacturers collectively produce vehicles at quality and price points that competitive Western manufacturers struggle to match. The Chinese government’s deliberate industrial policy — subsidies, infrastructure investment, supply chain integration, and export support — has produced a domestic EV industry that is now competing aggressively in international markets.

The pricing advantages of Chinese EVs are substantial and not easily replicable by Western competitors. BYD’s mass-market models offer features and range at price points 30 to 50 per cent below comparable Western vehicles. The cost advantage reflects a combination of vertically integrated supply chains (BYD produces its own batteries, semiconductors, and many other components), scale economies (Chinese EV manufacturers operate at production volumes that produce significant unit cost advantages), and lower input costs (lower labour costs and access to cheaper components). The cost advantage is real and structural rather than the result of unsustainable subsidies, though subsidy support has contributed historically.

Chinese EV manufacturers’ international expansion has been substantial. BYD’s European sales have grown to challenge Tesla’s position in the European EV market. The company has built manufacturing capacity in Thailand, Hungary, Brazil, and several other markets to serve regional demand without facing import tariffs. Chinese EV exports to emerging markets — Southeast Asia, Latin America, the Middle East, parts of Africa — have grown rapidly, often providing the first affordable EV options in markets where Western manufacturers have not focused.

The European Response

European automotive manufacturers — Volkswagen, BMW, Mercedes-Benz, Stellantis, Renault — have made substantial investments in electric vehicle capability and now offer competitive electric vehicles across their product ranges. The transition has been costly: legacy manufacturing infrastructure has had to be adapted or retired, workforce capabilities have had to be developed in different technical areas, and the financial returns on electric vehicle investments have not yet matched the returns of the internal combustion vehicles they are replacing.

The European Union’s regulatory framework — including the planned phase-out of internal combustion vehicle sales by 2035 and the carbon border adjustment mechanism affecting imports — has created strong incentives for European manufacturers to accelerate their EV transitions. Anti-dumping investigations against Chinese EV imports and tariff impositions have provided some protection for European manufacturers, though the long-term effectiveness of these measures against vertically integrated Chinese competitors with strong product offerings is uncertain.

Premium European brands — Porsche, BMW, Mercedes-Benz, Audi — have maintained competitive positions in higher-end EV segments where brand value and engineering quality justify pricing that mass-market Chinese competition does not directly threaten. The challenge for European manufacturers is more acute in the mass-market segment where Chinese price competition is most intense.

The American Adjustment

US automotive manufacturers — General Motors, Ford, Stellantis (which includes Chrysler and Jeep) — have made substantial commitments to electric vehicle transition but have experienced more difficulty than initially anticipated. EV losses have been substantial at these manufacturers, with GM and Ford both reporting EV business unit losses exceeding $5 billion in 2025. The strategic decisions about how aggressively to push EV transition versus maintaining profitable internal combustion vehicle production have become more complicated as EV demand growth has been more variable than initial projections suggested.

Tesla’s market position has compressed but remains substantial. The company continues to operate at margins that meaningfully exceed those of other US EV manufacturers, supported by manufacturing scale, software-led pricing optimisation, and the residual value of its brand position. The introduction of the Cybertruck has been commercially mixed but has not fundamentally affected the company’s market position. The Model 3 and Model Y continue as the highest-volume EVs in the US market, though both face increasing competitive pressure from new entrants (see our analysis in $5 Trillion Logistics Industry).

US policy support for EVs has been more variable than European support. The Inflation Reduction Act‘s tax credits for EV purchases and manufacturing have driven substantial investment in US-based EV production, but political uncertainty about the durability of these incentives has affected investment decisions. The exclusion of Chinese-made batteries and components from IRA-eligible vehicles has both protected US-based supply chain development and constrained the range of vehicles eligible for the credits (see our analysis in The Future of Energy).

The Battery Supply Chain Reality

Electric vehicle competition is fundamentally about battery technology and supply chain, and the global battery landscape has implications that extend beyond individual automotive companies. Chinese companies — CATL, BYD, CALB, EVE Energy — collectively manufacture approximately 70 per cent of global EV batteries, with CATL alone producing over a third of the global supply. The concentration creates both supply chain vulnerability for non-Chinese automotive manufacturers and strategic concerns for governments seeking energy security and industrial policy outcomes (see our analysis in The $1.3T Chip Economy).

The response has been substantial investment in non-Chinese battery production capacity. South Korean manufacturers — LG Energy Solution, Samsung SDI, SK On — have built capacity in the United States, Europe, and other markets. Japanese companies including Panasonic have expanded their US manufacturing in partnership with major automotive customers. European battery production capacity has grown through both Asian investment and domestic European efforts including Northvolt (which faced significant operational challenges) and various joint ventures.

Battery technology continues to evolve. Lithium iron phosphate (LFP) chemistry, which is cheaper and more durable than the nickel-manganese-cobalt chemistries that dominated earlier EVs, has become the standard for many mass-market vehicles. Solid-state batteries, long promised as a transformative technology, are approaching commercial production at multiple manufacturers, with Toyota and several Chinese manufacturers projecting commercial vehicles with solid-state batteries by 2027 to 2028. The energy density, charging speed, and safety improvements that solid-state batteries promise would meaningfully affect competitive positioning in the EV market.

Charging Infrastructure: The Differentiator

Charging infrastructure has emerged as a meaningful determinant of EV adoption and consequently of competitive position among EV manufacturers. Tesla’s Supercharger network was the first comprehensive fast-charging infrastructure deployed at scale, and it has been a significant competitive advantage. The opening of the Supercharger network to other vehicle manufacturers, while monetising the infrastructure investment, has also reduced the competitive advantage that the exclusive access provided.

Public charging infrastructure outside Tesla’s network has been built primarily by specialist operators — ChargePoint, Electrify America, EVgo, Ionity in Europe — and increasingly by traditional energy companies that see charging as a natural extension of their existing customer relationships. The pace of charging infrastructure deployment varies substantially across markets, with charging availability shaping consumer purchase decisions in ways that constrain EV adoption in markets where infrastructure has not been built out.

India’s EV Trajectory

India’s electric vehicle transition has progressed substantially but is structurally different from the transitions occurring in the United States, Europe, and China. The dominant Indian EV segment is two- and three-wheeled vehicles — scooters, motorcycles, and auto-rickshaws — which collectively account for the majority of Indian EV sales. Major Indian and international two-wheeler manufacturers — Bajaj, Hero MotoCorp, TVS, Ola Electric — have made substantial commitments to electric two-wheelers, supported by FAME-II subsidies and state-level incentives.

Indian four-wheel EV adoption has progressed more slowly but is accelerating. Tata Motors leads the Indian passenger EV market with affordable models that have established mainstream consumer acceptance. Mahindra has launched competitive EVs targeted at multiple market segments. Maruti Suzuki, which has dominated the Indian passenger vehicle market for decades, has been slower to enter EVs but is now committed to substantial EV launches. The Indian government’s production-linked incentive scheme for automotive and battery manufacturing has supported domestic EV capability development.

Strategic Implications

For business leaders, the evolution of the EV competitive landscape has implications across multiple dimensions. Companies in the automotive supply chain — semiconductor manufacturers, battery materials producers, charging infrastructure operators, automotive software developers — face strategic decisions about which manufacturers and which technology platforms to support. The decisions taken in the next two to three years will shape competitive positions for the subsequent decade as the EV transition progresses.

For corporate fleet operators, the economics of EV transition have shifted toward earlier adoption in many use cases. Total cost of ownership analysis increasingly favours electric vehicles in fleet applications, particularly where charging infrastructure can be deployed at fleet facilities and where operational profiles support electric vehicle range and charging characteristics. The competitive market among EV manufacturers has expanded the range of fleet-suitable vehicles available, supporting more flexible fleet electrification strategies.

The EV market that is emerging is more competitive, more global, and more technologically diverse than the Tesla-dominated market that existed five years ago. The companies that have positioned themselves to compete in this market — through manufacturing scale, supply chain control, software capability, and capital resources — are positioned to capture meaningful share of an industry that will define a substantial part of automotive economic activity for the foreseeable future. The companies that have not made these positioning investments will find competitive position increasingly difficult to defend.