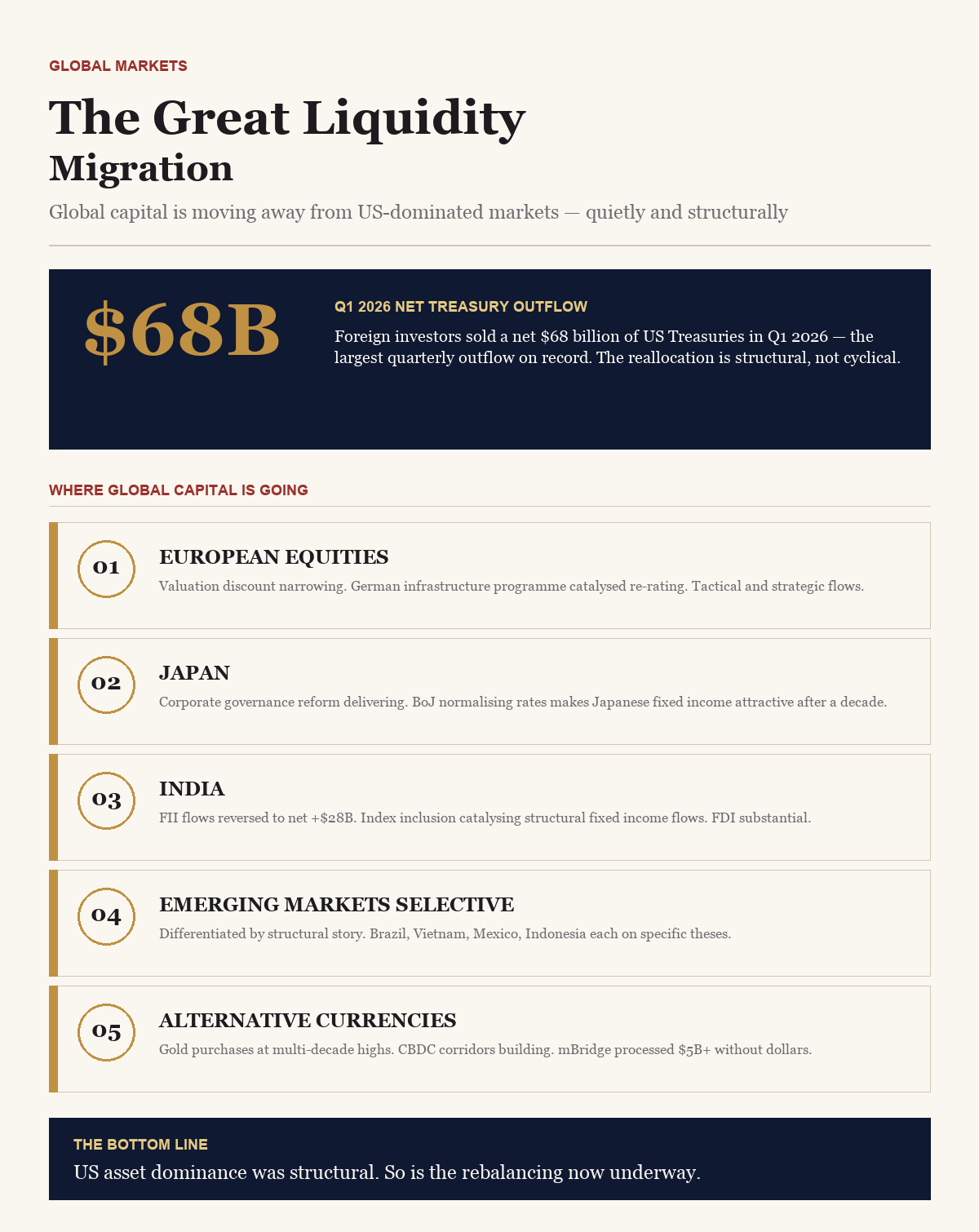

In the first quarter of 2026, foreign investors sold a net $68 billion of US Treasury securities — the largest quarterly net outflow since records began. Simultaneously, equity funds tracking European markets recorded their largest quarterly inflows in eleven years. The Indian rupee and Brazilian real both strengthened against the dollar despite conventional expectations that a period of global risk aversion would drive capital back to the traditional safe haven of US assets. These are not random data points. They are signals of a structural shift in where global capital wants to be — and where it no longer wants to be.

The great liquidity migration is not a single event with a clear start date. It is a collection of overlapping forces that have been building for several years and are now reinforcing each other with sufficient momentum to alter benchmark allocations at the world’s largest institutions. Understanding those forces — and the destinations attracting the capital being redirected — requires examining changes in reserve management, institutional allocation, private capital flows, and the geopolitical signals that are reshaping investment calculus at sovereign and institutional levels.

The Dollar’s Wobble and Reserve Diversification

The US dollar remains the world’s dominant reserve currency, accounting for approximately 57% of global foreign exchange reserves as measured by the IMF’s COFER database. That figure represents a structural share that has declined from 71% in 2000 — a slow but consistent erosion that has accelerated in the post-2022 period following the weaponisation of dollar-based financial infrastructure against Russia.

The freezing of approximately $300 billion in Russian central bank assets held in Western financial systems following Russia’s 2022 invasion of Ukraine was, for many central banks, a proof of concept for a risk they had previously treated as theoretical. Holding reserves in US Treasuries or dollar-denominated instruments means accepting that those assets can be frozen or seized if relations with the United States deteriorate. That is not a risk that China, Saudi Arabia, India, or dozens of other countries whose foreign policy does not perfectly align with Washington can dismiss.

The response has been measured but unmistakable. Central bank gold purchases have been at multi-decade highs for three consecutive years. The People’s Bank of China has reduced its disclosed US Treasury holdings from a peak of $1.3 trillion in 2013 to approximately $760 billion — a reduction that has been absorbed by the market without drama but represents a sustained policy of diversification. Saudi Arabia’s Public Investment Fund has accelerated deployment into non-dollar assets across European equities, Asian infrastructure, and tokenised financial instruments.

Where the Institutional Money Is Going

Among private institutional investors — pension funds, endowments, sovereign wealth funds, and insurance companies — the reallocation is being driven by a combination of valuation, return expectations, and explicit diversification mandates.

European equities have been the primary beneficiary of US reallocation in 2025 and into 2026. Relative valuations drove the initial interest: European equities traded at a roughly 35% discount to US equities on a price-to-earnings basis entering 2025, a gap that had widened through the US technology-led bull market of 2023 and 2024. As that valuation differential became difficult to justify on fundamentals, tactical and then strategic capital began rotating. Germany’s historic €500 billion infrastructure investment package — announced in March 2025 — catalysed a rerating of German and broader European industrial equities that attracted both momentum-following and value-oriented institutional capital.

Japan has been another significant destination. The Tokyo Stock Exchange’s corporate governance reform campaign — pressuring companies to reduce cross-shareholdings, increase return on equity, and adopt more shareholder-friendly capital policies — has continued to produce results visible in earnings trends and buyback volumes. The Bank of Japan‘s gradual exit from its yield curve control policy has removed a structural distortion from Japanese bond markets and made Japanese fixed income more attractive to global allocators for the first time in over a decade.

Emerging markets, as a category, have attracted more differentiated flows. The era of the undifferentiated ‘EM allocation’ driven by commodity exposure and demographic growth narratives has given way to a more selective approach. India, Vietnam, Mexico, and Indonesia are attracting capital on the basis of specific structural stories: manufacturing supply chain diversification, technology sector development, and domestic consumption growth. Brazil, which has benefited from commodity demand and political stabilisation, is attracting interest from investors seeking commodity exposure with improving governance characteristics.

India’s Moment in the Capital Migration

India’s position in the global capital migration deserves particular attention. The country has benefited from multiple converging forces that are directing institutional capital flows — and from a policy environment that, with some notable exceptions, has been more receptive to foreign capital than at any previous point in its economic history (see our analysis in The IPO Window Reopens).

Foreign institutional investment in Indian equities reached a net $28 billion in the financial year to March 2026, reversing two years of significant outflows driven by rising global rates and dollar strength. The reversal reflects a reassessment by global allocators: India’s GDP growth of approximately 6.8% in FY2026, combined with improving corporate earnings quality and a financial system that has substantially cleaned up its non-performing loan problem, makes the fundamental investment case stronger than at any point since 2014 (see our analysis in The Powell Succession Crisis).

The inclusion of Indian government bonds in JPMorgan‘s GBI-EM Global Diversified Index — implemented in phases from June 2024 — is directing a structural flow of passive institutional capital into Indian fixed income. The estimated passive inflow associated with index inclusion is $25-40 billion over the implementation period, an amount that would have materially pressured the rupee to appreciate if RBI had not partially offset it through reserve accumulation. Bloomberg Barclays is expected to complete its own Indian bond index inclusion by end-2026, adding another tranche of structural demand (see our analysis in Inflation’s Persistence).

The supply chain diversification investment flowing into Indian manufacturing — semiconductors, electronics, pharmaceuticals, textiles — represents a different category of capital: foreign direct investment with long holding periods and genuine economic integration. Apple’s accelerated iPhone assembly expansion, Foxconn’s broader manufacturing investments, and Samsung‘s display and memory manufacturing discussions collectively represent multi-billion dollar commitments that will remain regardless of short-term market conditions (see our analysis in Real Estate in a High-Rate World).

Private Capital and the Alternatives Expansion

Alongside the shift in public market allocations, there is an equally significant migration of capital into private markets across non-US geographies. Global private equity fundraising was dominated by US-focused strategies for most of the past two decades. That concentration is shifting as large LPs — sovereign wealth funds, pension systems, endowments — seek both diversification and return premium in markets where private equity penetration is lower and therefore the opportunity set is less efficiently priced.

India-focused private equity and venture capital attracted approximately $12 billion in 2025 — down from the 2021 peak of $38 billion but representing a stabilisation after two years of sharp correction and a return to deployment on more disciplined valuations. Southeast Asia, which attracted significant capital during the 2020-2022 technology boom, has seen a correction similar to India’s but is beginning to see renewed interest in infrastructure and financial services deals where valuations are more defensible.

Infrastructure as an asset class has been a particular beneficiary of the capital migration narrative. The combination of global decarbonisation investment requirements, nearshoring-driven logistics and manufacturing infrastructure needs, and the defensive cash flow characteristics of infrastructure in a higher-rate environment has made the asset class attractive to a broader investor base than ever before. Infrastructure funds focused on Asia, the Middle East, and Africa are fundraising successfully against a backdrop of strong LP interest that would have been difficult to generate five years ago.

The Geopolitical Dimension

Underlying the financial flows is a geopolitical reorganisation that is reshaping the architecture of international capital. The US-China strategic competition, the expansion of BRICS to include Saudi Arabia, the UAE, Egypt, Iran, Ethiopia, and Argentina, and the broader effort by non-Western economies to create financial infrastructure that is less dependent on dollar rails — these are not primarily financial decisions, but they have profound financial consequences.

The mBridge project — a central bank digital currency platform connecting China, Hong Kong, Thailand, and the UAE — has processed over $5 billion in cross-border transactions without touching the US dollar or Swift. While still small relative to global FX volumes, it demonstrates that the infrastructure for a parallel international payment system is functional and being actively developed. For institutional investors assessing currency and geopolitical risk exposures, the maturation of dollar-alternative financial infrastructure is a scenario that must be modelled, even if its probability of widespread adoption within a five-year horizon remains uncertain.

What This Means for Portfolio Strategy

For institutional investors whose strategic asset allocation was built around US equity and bond market dominance, the great liquidity migration requires a fundamental review of geographic diversification. Benchmark weights that make sense when US markets represent 65% of global market capitalisation may need revision as relative performance and growth dynamics shift. The performance of European equities in 2025 and 2026 — which outpaced US equities by approximately 18 percentage points in local currency terms — has already prompted many large institutions to review their geographic weights.

Currency strategy becomes more complex in a world of multipolar capital flows. The dollar’s reserve currency status provides a hedge during risk-off events, but the correlation between risk aversion and dollar strength has weakened in 2026 in ways that investors relying on that historical relationship are finding disorienting. Explicit currency risk management — hedged share classes, cross-currency swaps, local currency denominated instruments — becomes more important when the traditional reserve currency safe haven assumption is less reliable.

The great liquidity migration is not a trend that will reverse quickly. The structural forces driving it — dollar weaponisation risk, US valuation premiums, geopolitical fragmentation, and the maturation of alternative investment destinations — have been building for years and are reinforcing rather than offsetting each other. Institutions that respond to these signals with measured, deliberate portfolio repositioning will be better placed than those that wait for the shift to become undeniable before acting. In capital markets, by the time a trend is undeniable, the positioning opportunity has largely passed.