The temptation when writing about quantum computing is either to overstate its imminence or to dismiss it as decades from commercial relevance. Both framings miss what is actually happening. The technology is making genuine and rapid progress, with milestones in 2024 and 2025 that several years ago would have been considered optimistic projections for 2030 or later. At the same time, the gap between current quantum hardware capabilities and the requirements for solving most commercially relevant problems remains substantial, and bridging that gap will take more time and capital than the most enthusiastic predictions assume. The right framing for business leaders is neither hype nor dismissal but specific assessment: what is the technology actually capable of today, what is the credible timeline for capability expansion, and which industries face quantum exposure that warrants strategic attention now.

Where Quantum Computing Stands in 2026

The most consequential development in quantum computing over the past two years has been progress on quantum error correction. Quantum computers are fundamentally noisy systems in which individual quantum bits (qubits) accumulate errors rapidly during computation. Useful quantum computing requires error correction techniques that allow logical qubits to maintain coherent states across many physical qubits, and the engineering of these error correction systems has been one of the central challenges of practical quantum computing.

Google’s Willow processor, announced in late 2024, demonstrated below-threshold error correction for the first time — meaning that adding more physical qubits actually reduced rather than increased the error rate of logical operations. This was a significant milestone that demonstrated a path to fault-tolerant quantum computing, even though Willow itself contains a relatively small number of qubits. Similar progress has been demonstrated by IBM, Quantinuum (using trapped-ion technology), and PsiQuantum (using photonic approaches), suggesting that quantum error correction is now an active engineering challenge rather than a theoretical obstacle.

The path from error-corrected demonstration systems to commercially useful quantum computers remains long. Most credible roadmaps from major quantum computing companies project useful, large-scale quantum advantage in specific applications by 2028 to 2032, with broader commercial relevance emerging over the subsequent five to ten years. These timelines are aggressive enough that the technology cannot be safely ignored by industries where quantum impact is plausible, but they are not so imminent that business strategy needs to be rebuilt around quantum capabilities arriving in 2027.

Industries With Genuine Near-Term Exposure

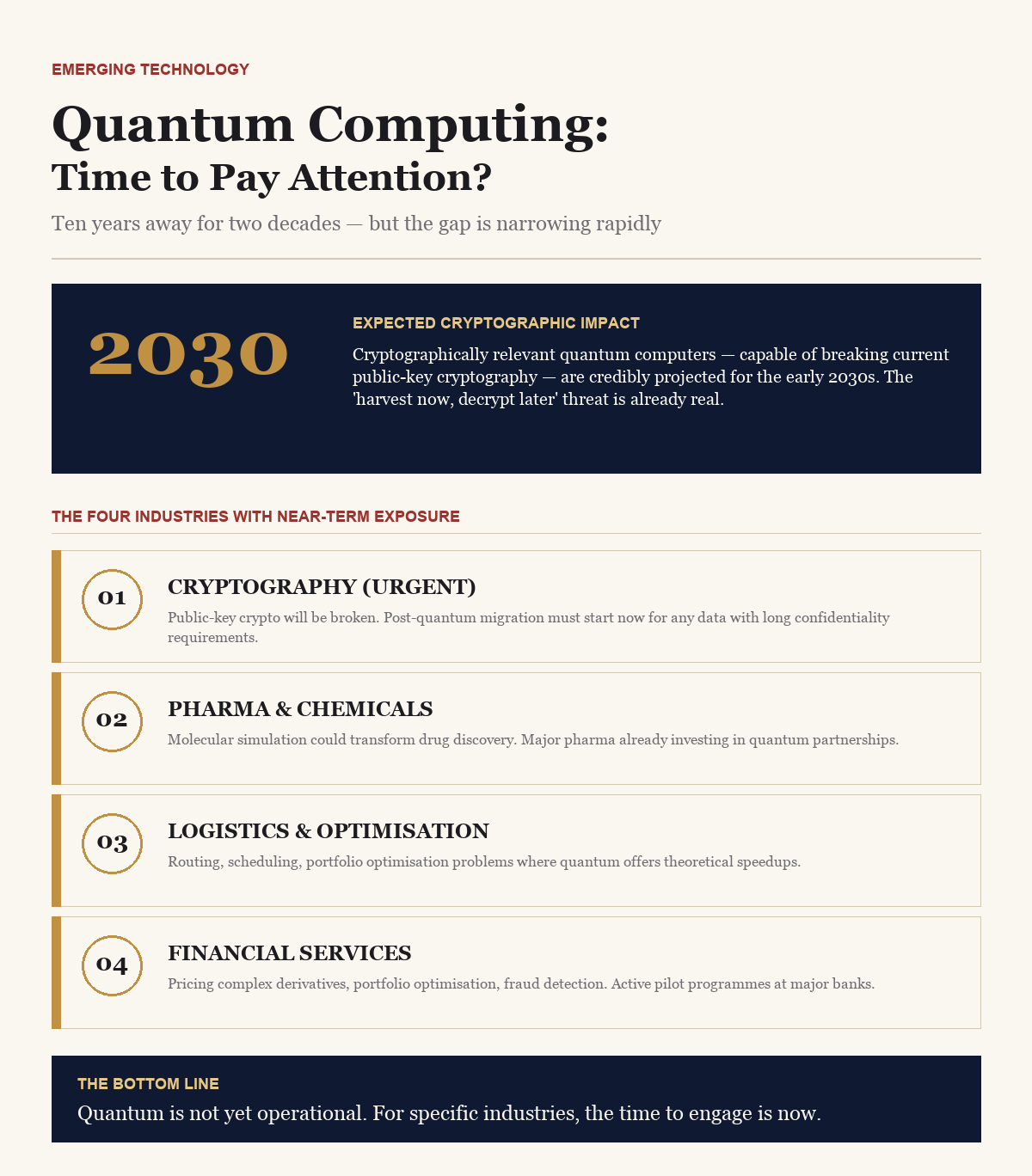

Three industries face quantum computing exposure that should be on the strategic agenda now, even though full quantum advantage remains years away. Cryptography is the most acute and time-sensitive case. Current public-key cryptographic systems — including RSA and elliptic curve cryptography that secure most digital communications, financial transactions, and stored data — would be broken by sufficiently powerful quantum computers running Shor’s algorithm. The exact timeline for this ‘cryptographically relevant’ quantum computer is debated but generally projected for the 2030s.

The cryptographic transition has already begun. The US National Institute of Standards and Technology finalised its first post-quantum cryptographic standards in 2024, providing approved algorithms that are resistant to quantum attacks. Major technology companies and governments have begun migrating critical systems to post-quantum cryptography. The ‘harvest now, decrypt later’ threat — adversaries capturing encrypted data today to decrypt with future quantum computers — is real and is driving urgent migration for organisations handling sensitive information with long confidentiality requirements. Financial services, defence, healthcare, and intellectual property-intensive businesses face this risk most directly.

Pharmaceutical and chemical industries face exposure through quantum simulation. Drug discovery and molecular design involve solving quantum mechanical problems that classical computers approximate imperfectly. Quantum computers, in principle, can simulate molecular systems exactly, potentially accelerating drug discovery, materials development, and chemical engineering significantly. Pharmaceutical companies including Roche, AstraZeneca, Bristol-Myers Squibb, and chemical companies including BASF and Dow have invested in quantum computing partnerships and pilots, recognising that the technology, when it arrives at commercial scale, will affect competitive positions in their industries materially.

Logistics and optimisation-intensive industries face a third category of quantum exposure. Optimisation problems — vehicle routing, supply chain configuration, portfolio optimisation, network design — are computationally expensive and increasingly important to operational efficiency. Quantum algorithms for certain optimisation problems offer potential speedups that, if realised at scale, would provide significant competitive advantages. The timeline for commercially meaningful quantum optimisation is debated, but the potential is sufficient that logistics-intensive businesses should be monitoring the technology and considering pilot engagements.

The Companies Building the Technology

The competitive landscape in quantum computing has evolved substantially. IBM has built one of the most extensive quantum computing platforms with its quantum hardware and the Qiskit software ecosystem. Google has pursued advanced superconducting qubit technology with significant research investment. Microsoft, after years of investment in topological qubit research, has shifted toward a more diverse approach including partnerships with multiple hardware approaches. Amazon Web Services has launched Braket, providing access to quantum hardware from multiple providers through its cloud platform (see our analysis in From GPU Monoculture to Chiplets).

Beyond the major cloud providers, specialised quantum computing companies have built significant capabilities. IonQ uses trapped-ion technology to produce high-fidelity quantum operations. Rigetti has pursued superconducting qubit systems with a focus on commercial cloud delivery. PsiQuantum is building photonic quantum computers at scale. Quantinuum (formed from the combination of Honeywell Quantum Solutions and Cambridge Quantum) combines hardware and software with a focus on near-term applications. The diversity of technical approaches reflects ongoing uncertainty about which quantum computing technology will prove most successful at scale (see our analysis in The $1.3T Chip Economy).

Chinese quantum computing companies, including the state-backed efforts at the University of Science and Technology of China and private companies like Origin Quantum, have made significant progress and represent a credible alternative to the predominantly American and European quantum ecosystem. The geopolitics of quantum computing are now meaningful, with export controls and technology competition factors that will shape commercial development (see our analysis in Cryptocurrency Regulation).

Practical Steps for Business Leaders

For business leaders considering how to engage with quantum computing, the appropriate response depends on industry and time horizon. For industries with cryptographic exposure — which now includes essentially every business handling sensitive data — the priority is post-quantum cryptography migration. The migration is technically complex and operationally significant, requiring identification of current cryptographic dependencies, evaluation of post-quantum alternatives, and phased deployment that maintains security throughout the transition. This work should be underway in any organisation handling sensitive data with long confidentiality requirements.

For industries with substantive quantum simulation or optimisation exposure, the appropriate engagement is exploratory pilot work that develops internal capability and external partnership infrastructure. The objective is not to deploy quantum computing in production today — the hardware is not ready for most production workloads — but to build the organisational understanding, partnership relationships, and talent base that will enable serious deployment when the technology matures. Companies that wait until quantum computing is clearly commercially viable will be three to five years behind competitors that engaged earlier.

For industries without specific quantum exposure, the appropriate engagement is monitoring rather than active development. Quantum computing developments should be tracked at the level of awareness of major milestones, but resources should not be diverted to quantum-specific activities. The technology will become commercially relevant for these industries, but the timeline is sufficiently long that earlier engagement does not produce competitive advantage. The risk for these businesses is over-investment in a technology that is not yet productively deployable rather than under-investment.

The Quantum Talent Question

Talent availability is a meaningful constraint on quantum computing’s broader development. The global population of physicists, computer scientists, and engineers with deep quantum computing expertise is small, and the demand from major quantum computing companies, research institutions, and corporate quantum initiatives substantially exceeds supply. The shortage has implications for any business considering serious quantum engagement: the talent required to drive a quantum initiative will be expensive and difficult to recruit, and the pace of organisational quantum capability development will be constrained by talent availability more than by technology access.

The talent pipeline is improving but slowly. Major universities have expanded quantum computing programmes, and quantum-specific PhD programmes are graduating larger cohorts. National quantum initiatives in the United States, the European Union, the United Kingdom, and several Asian countries have provided funding that supports talent development. But the timeline from increased programme capacity to deployable industrial talent is years, and the global talent market for quantum computing expertise will remain tight throughout the late 2020s.

Conclusion: Calibrated Attention

Quantum computing is real, is progressing meaningfully, and is approaching commercial relevance in specific industries. The appropriate executive response is calibrated attention proportionate to the industry’s specific exposure rather than blanket enthusiasm or dismissal. The cryptographic transition is urgent for any business handling sensitive data. Pharmaceutical, chemical, materials, and logistics businesses should be engaging exploratorily with the technology. Most other businesses can monitor developments without immediate operational action.

The pattern of technology adoption that follows transformative technologies suggests that the businesses that will benefit most from quantum computing are those that engage early enough to build organisational capability before the technology matures, but not so early that they waste resources on capabilities that cannot be productively deployed for years. Identifying the right level of engagement for a specific business requires judgement about industry-specific quantum exposure rather than general technology fashion. That judgement should now be on the strategic agenda of every business of meaningful scale.