Energy markets have a peculiar relationship with geopolitical risk: they price it intensely in the short term and discount it almost entirely in the long term. When Iran seized a Marshall Islands-flagged tanker in the Strait of Hormuz in April 2026, oil futures spiked 8% within hours. When the tanker was released three days later without incident, roughly half that spike unwound. Traders moved on. Energy analysts updated their models. The underlying risk — that 20% of global oil supply transits a strait that a hostile regional power has the technical capability and stated willingness to disrupt — remained exactly as it was before the incident and after it.

For corporate treasuries, procurement teams, and CFOs managing energy-exposed businesses, this short-termism in market pricing is both a risk and an opportunity. The risk is that routine market function creates a false sense of security: because Hormuz has not been physically closed since the tanker war of the 1980s, it is easy to assume it will not be. The opportunity is that the persistent underpricing of tail risk in energy markets creates hedging opportunities for businesses willing to think in longer time horizons than commodity traders.

The Strait’s Strategic Anatomy

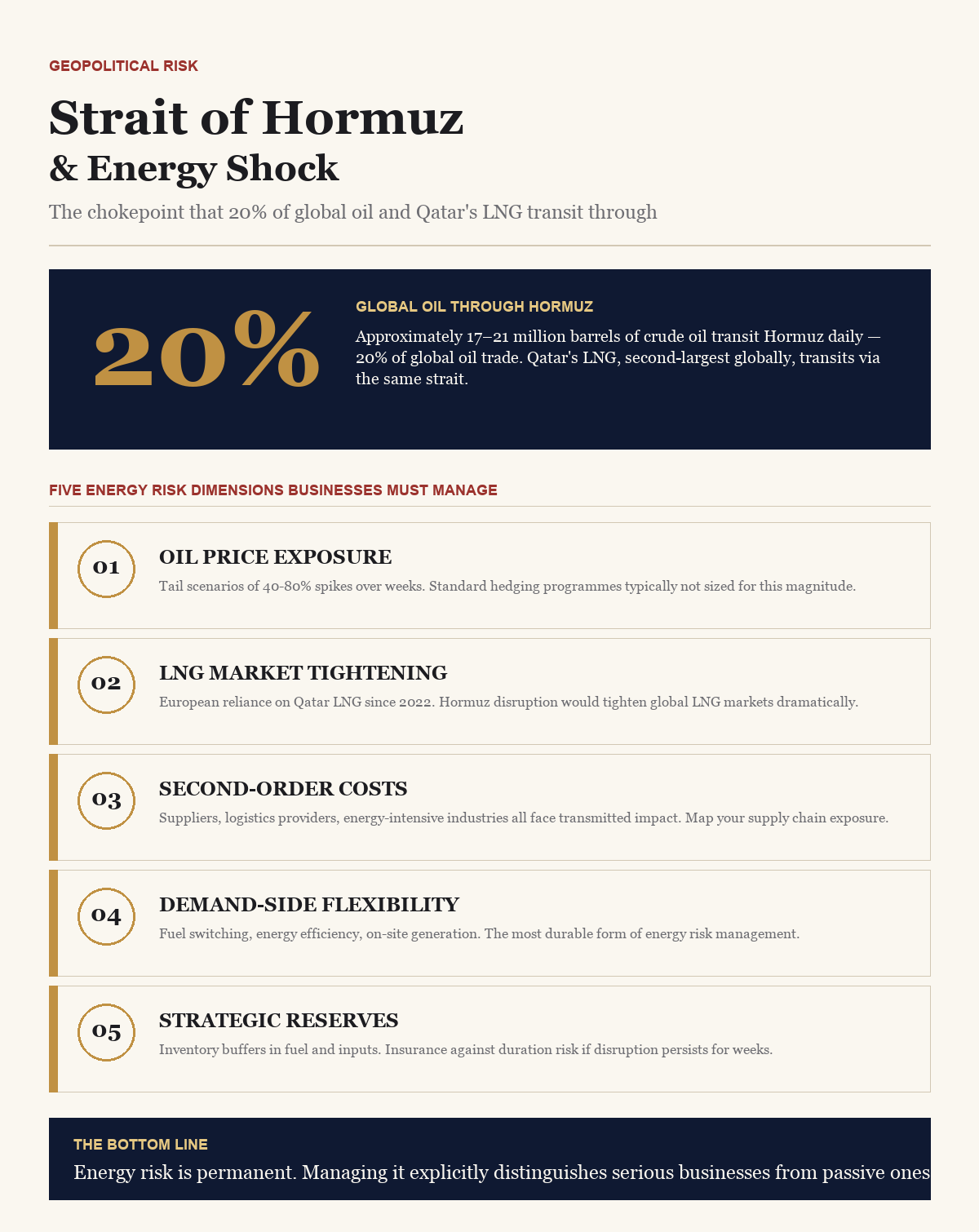

Understanding why the Strait of Hormuz matters requires understanding the flow of energy through it. On any given day, 17 to 21 million barrels of crude oil transit the strait — primarily from Saudi Arabia, Iraq, the UAE, Kuwait, and Iran itself. Qatar’s LNG exports — the second largest in the world, supplying Europe, Japan, South Korea, and India — transit the strait via the Qatari port of Ras Laffan. The strait is the single exit point for Persian Gulf energy production, and there is no scalable alternative. The East-West Pipeline across Saudi Arabia, which can carry approximately 5 million barrels per day to the Red Sea port of Yanbu, provides partial mitigation but covers roughly a quarter of normal Hormuz volumes at maximum capacity.

Iran’s capability to threaten Hormuz transit is not in dispute. The Islamic Revolutionary Guard Corps Navy operates a substantial fleet of fast attack craft, submarine capabilities, shore-based anti-ship missile systems, and naval mines that could impose significant costs on tanker traffic transiting the strait. The IRGCN has conducted repeated exercises demonstrating these capabilities, seized commercial vessels in disputed legal actions, and attacked tankers with limpet mines during the 2019-2020 escalation cycle. The capability to disrupt, if not fully close, Hormuz shipping is well-demonstrated.

The 2026 Escalation: What Happened and Why

The April 2026 escalation in the Strait of Hormuz was triggered by a combination of factors that had been accumulating since late 2025. US reimposition of maximum pressure sanctions on Iranian oil exports — targeting Iranian crude purchases by Chinese refineries through secondary sanctions on Chinese financial institutions — reduced Iran’s oil export revenues by an estimated $18 billion annually from their 2024 levels. Iranian leadership, facing domestic economic pressure and a presidential election cycle, responded with a series of escalating provocations: harassment of commercial vessels, threats to close the strait, and the April tanker seizure.

Oil markets responded to the escalation with the $105 price spike that briefly repriced global energy. The wider economic consequences were visible in inflation data: US CPI for April 2026 showed a 0.4% month-on-month increase in the energy component, reversing a six-month trend of decline. European energy prices, already sensitive to supply disruption given the post-Ukraine restructuring of gas supply, spiked more dramatically. Brent-WTI spreads widened. LNG spot prices, which had been trading near their lowest levels since 2021, jumped 40% in a week.

The episode ended when backchannel negotiations — facilitated by Oman, which maintains unique diplomatic relationships with both Washington and Tehran — produced a temporary de-escalation understanding. Iran received informal assurances that secondary sanctions enforcement would not target certain financial institutions; the US received assurances that tanker harassment would cease. The fragility of this arrangement, dependent on informal understandings between governments with fundamentally opposed interests, was not lost on market participants.

Structural Vulnerability: The LNG Dimension

The oil price implications of Hormuz disruption receive most of the attention, but the LNG dimension is arguably more consequential for specific economies and businesses. Qatar, the world’s second-largest LNG exporter, ships all of its LNG through the strait. Europe — which increased Qatar LNG imports significantly after the 2022 reduction of Russian gas supplies — is structurally exposed to Hormuz disruption in its gas supply. Japan and South Korea, which import the majority of their LNG from Persian Gulf sources, face acute vulnerability (see our analysis in The Great Liquidity Migration).

For Indian businesses, the LNG exposure is growing. India has been rapidly expanding LNG import terminal capacity as domestic gas demand grows in fertiliser production, city gas distribution, and industrial applications. The Petronet LNG terminal at Dahej, the Shell terminal at Hazira, and the newer terminals at Mundra and Ennore collectively handle volumes that are growing at approximately 8% annually. A sustained Hormuz disruption would tighten LNG markets globally and drive spot prices to levels that would render gas-dependent Indian industrial processes uneconomic at current product pricing (see our analysis in Doing Business in the Age of Sanctions).

Saudi Arabia’s Strategic Calculations

Saudi Arabia’s response to Hormuz risk is itself a market variable that businesses need to model. Saudi Aramco maintains the world’s largest strategic spare production capacity — estimated at 1.5 to 2 million barrels per day — specifically as a buffer against supply disruption. In the event of a partial Hormuz disruption, the activation of spare capacity and the East-West pipeline would partially offset reduced throughput, but not completely. Saudi Arabia has also been investing in expanded refinery capacity that could divert some crude volumes to products that can transit alternative routes (see our analysis in Supply Chain Sovereignty).

Saudi Arabia’s relationship with Iran — which has oscillated between hostility and cautious normalisation since the Chinese-brokered rapprochement of 2023 — adds another variable. A Saudi-Iranian détente that reduces regional tensions would lower Hormuz risk; a deterioration of that relationship would raise it. The April 2026 episode tested the resilience of the 2023 normalisation and found it relatively durable at the state level, even as IRGCN provocations continued — a distinction that reflects the complexity of Iranian political factions and their relationship to official policy.

Energy Risk Management for Businesses

The practical implication of Hormuz risk for businesses is not that they should assume a closure is imminent — it is not — but that energy cost volatility driven by Middle East geopolitics is a permanent feature of the operating environment that should be managed explicitly rather than absorbed as a surprise. Three dimensions of energy risk management are most relevant.

Fuel and energy hedging programmes need to incorporate tail scenarios that include significant supply disruption, not just price volatility within normal ranges. Most corporate hedging programmes are designed around price volatility of plus or minus 20-30%; a Hormuz disruption could produce price moves of 40-80% over weeks or months. Hedging coverage, duration, and instrument selection should be calibrated to those scenarios for businesses where energy is a material cost component.

Supply chain energy dependency mapping — identifying which suppliers and logistics providers are most exposed to energy cost spikes — allows businesses to anticipate second-order impacts before they materialise. A logistics provider heavily dependent on bunker fuel, a fertiliser manufacturer dependent on natural gas, a chemical company using Persian Gulf feedstocks: each of these represents a transmission channel through which Hormuz disruption reaches businesses that do not directly consume oil or LNG.

Demand-side flexibility — the ability to substitute energy sources, adjust production timing, or modify product specifications in response to energy cost changes — is the most durable form of energy risk management but also the most capital-intensive to develop. Businesses investing in energy efficiency, fuel switching capability, or on-site renewable generation are building structural resilience that pays dividends across multiple scenarios, not just Hormuz-specific events.

The Outlook

The structural conditions that make the Strait of Hormuz a persistent risk — Iran’s sanctions-driven incentive to threaten disruption, the absence of scalable alternative transit routes, and the concentration of global energy supply in a small geographic area — are not going to change in the near term. The energy transition will eventually reduce the strategic significance of Persian Gulf oil and gas, but that transition is measured in decades, and in the meantime global dependence on Hormuz transit is, if anything, increasing as developing economy energy demand grows.

The April 2026 episode will not be the last time that Middle East tensions cause energy price spikes that create inflationary pressure, disrupt supply chains, and test the resilience of energy-dependent businesses. The question for business leaders is whether that risk is being managed with the same rigour applied to other material business risks — or whether it is still being treated as background geopolitical noise that someone else worries about. In 2026, that distinction has a direct line to the P&L.