When Apple announced in early 2024 that it had assembled $14 billion worth of iPhones in India in the prior fiscal year — approximately 14% of its global iPhone production — the story travelled fast. It was the kind of concrete, brand-name validation that a narrative needs to cross from aspiration to credibility. When Samsung, Foxconn, and a roster of Taiwanese electronics manufacturers followed with their own India investment announcements, the momentum seemed self-reinforcing. Morgan Stanley projected India’s manufacturing exports could reach $1 trillion annually by 2028. The World Bank cited India as the most promising manufacturing destination after China.

That narrative is not wrong. India’s manufacturing sector is growing, its infrastructure is improving, and its production-linked incentive programme has successfully attracted investment in sectors from semiconductors to pharmaceuticals to electronics. But the gap between India’s manufacturing ambitions and its current capabilities is wide, and the obstacles between here and there are more structural than the promotional literature tends to acknowledge. For business leaders evaluating India as a manufacturing base, the honest assessment requires engaging with both the opportunity and the constraint.

What Has Actually Been Achieved

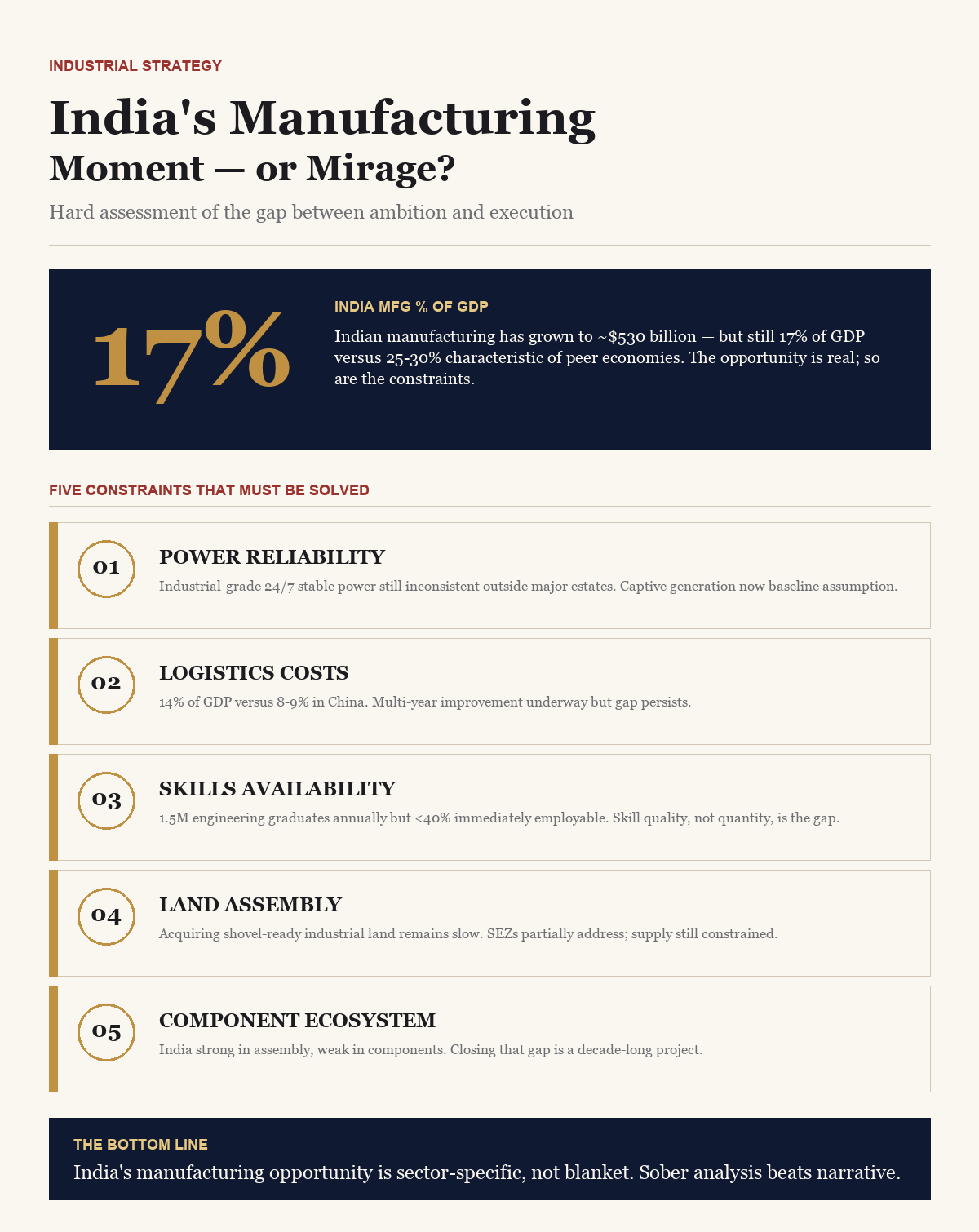

India’s manufacturing output has grown from approximately $300 billion in 2014 to an estimated $530 billion in 2025 — significant growth, but still representing about 17% of GDP, well below the 25-30% that characterises economies at comparable development stages. The production-linked incentive scheme, launched in 2020 across 14 sectors, has disbursed approximately $3.5 billion in incentives and attracted committed investments of over $20 billion. Electronics manufacturing — particularly mobile phones — has been the standout success, with India becoming the world’s second-largest smartphone manufacturer by volume.

Infrastructure has improved materially, albeit unevenly. The National Infrastructure Pipeline, a $1.4 trillion investment programme running through 2025, has delivered measurable improvements in road connectivity, port capacity, and power supply reliability. The Delhi-Mumbai Industrial Corridor and similar dedicated freight corridor projects have created logistics infrastructure comparable in quality to Southeast Asian standards in the corridors they serve. Digital infrastructure — the Aadhaar identity system, the Unified Payments Interface, the Open Network for Digital Commerce — provides a foundation for supply chain integration that many competing manufacturing destinations lack.

The pharmaceutical sector illustrates what Indian manufacturing does well. India supplies approximately 20% of global generic medicine volumes and is the primary supplier to the WHO’s Essential Medicines programme. Indian pharmaceutical manufacturing has achieved quality certification from the US FDA, the EU’s EMA, and stringent regulatory bodies across 200 markets. This is not low-cost assembly; it is technically sophisticated manufacturing built over decades of investment in chemistry, process engineering, and quality management.

The Infrastructure Gap That Remains

Outside the dedicated industrial corridors and the major metropolitan areas, India’s physical infrastructure constrains manufacturing competitiveness in ways that benchmarking studies consistently document. Power supply reliability is the most frequently cited operational challenge: despite significant improvements, industrial-grade power supply — stable voltage, minimal interruptions, 24/7 availability — remains inconsistent in many manufacturing locations outside the major industrial estates. Manufacturers operating in India typically invest in captive power generation as a baseline precaution, adding capital cost that competing locations do not require.

Logistics costs as a percentage of GDP — a standard measure of supply chain efficiency — stand at approximately 14% in India, compared to 8-9% in China and 6-7% in the United States. That differential reflects a combination of road quality outside major corridors, port handling efficiency, customs clearance times, and last-mile connectivity. For manufacturers whose competitiveness depends on just-in-time supply chain management, the logistics cost premium is a meaningful factor in location decisions. The gap is narrowing — logistics costs as a percentage of GDP have declined from approximately 18% a decade ago — but it has not closed.

Water availability is a growing constraint that receives less attention than power but is equally critical for many manufacturing processes. India’s water stress map — published by the World Resources Institute — shows significant portions of the most attractive manufacturing geographies, including Gujarat, Rajasthan, and parts of Tamil Nadu, facing high or extremely high water stress. Semiconductor fabrication, textiles, food processing, and chemicals all require reliable water supply. Climate change is intensifying water stress across the Indian subcontinent, and water risk needs to be explicitly modelled in manufacturing location decisions.

The Labour Equation: Demographic Dividend or Skills Deficit?

India’s demographic profile — approximately 65% of the population below 35 years of age, with roughly 10 million new workforce entrants annually — is routinely cited as a structural advantage for labour-intensive manufacturing. The labour cost comparison is real: average manufacturing wages in India are approximately 20-25% of Chinese levels in comparable sectors, and significantly below Vietnam and Thailand. For labour-intensive assembly — electronics, garments, footwear — that differential matters (see our analysis in India’s Startup Ecosystem).

The skills availability picture is more complicated. India produces approximately 1.5 million engineering graduates annually, the second-largest engineering graduate output in the world. But the quality distribution is highly uneven: surveys by the National Employability Report consistently find that fewer than 40% of engineering graduates are immediately employable in technical roles without further training. The mismatch between formal educational credentials and practical industrial skills is a structural problem that the Indian education system has not resolved, despite multiple government initiatives (see our analysis in Supply Chain Sovereignty).

Labour relations and flexibility are additional considerations. India’s Industrial Disputes Act and related labour legislation have historically made workforce adjustments — scaling down production, changing shift patterns, redeploying workers — more legally complex than in competing manufacturing destinations. Labour law reforms at the state level, and the consolidation of central labour laws into four codes (though implementation remains incomplete), have improved the framework, but navigating labour relations in India still requires more legal and HR infrastructure than comparable operations in Vietnam or Bangladesh (see our analysis in China+1 Supply Chain).

The Regulatory and Ease of Doing Business Reality

India’s ranking on the World Bank’s Ease of Doing Business index improved dramatically between 2014 and 2020, rising from 142nd to 63rd — a genuine achievement that reflected real improvements in registration processes, construction permit timelines, and tax compliance simplification. The index was discontinued after 2020, removing the annual accountability mechanism that had driven those improvements. Anecdotal evidence from investors and manufacturers operating in India suggests that ease of doing business has continued to improve in some dimensions and stagnated in others (see our analysis in $5 Trillion Logistics Industry).

Land acquisition remains the most consistent operational challenge cited by manufacturing investors. India’s Land Acquisition Act requires lengthy consent and compensation processes for large-scale industrial land assembly. State industrial development corporations have partially addressed this through pre-assembled industrial parks and Special Economic Zones, but the supply of shovel-ready, large-parcel industrial land with reliable utilities in desirable locations is constrained relative to demand. The gap between announced investments and actually deployed capital in Indian manufacturing reflects, in significant part, the difficulty of moving from commitment to construction.

The Sectoral Opportunities That Are Real

Despite the structural challenges, specific sectors present genuinely compelling manufacturing opportunities in India that are not available at comparable cost and scale elsewhere. Generic pharmaceuticals and active pharmaceutical ingredients represent India’s most established manufacturing advantage — deep talent pools, proven quality systems, and regulatory relationships that would take competitors decades to replicate. The API supply chain vulnerability exposed during COVID-19 has accelerated domestic manufacturing investment in this sector, creating both government incentives and commercial demand for expanded capacity.

Electronics assembly — particularly for export-oriented production in smartphones, laptops, and consumer devices — has established real momentum. The production-linked incentive structure for mobile manufacturing has demonstrated that India can attract and retain large-scale electronics production, though the component ecosystem (displays, batteries, semiconductors) that makes Chinese electronics manufacturing so efficient still needs to develop. India is currently strong in final assembly; it is weak in components. Closing that gap is a decade-long project.

Renewable energy equipment manufacturing presents a specific opportunity tied to India’s ambitious domestic solar and wind installation targets. India has deployed significant domestic solar module manufacturing capacity and is developing wind turbine and battery storage manufacturing. The domestic demand base — India is targeting 500 gigawatts of renewable capacity by 2030 — provides the volume anchor that manufacturing scale requires.

The Honest Assessment

India’s manufacturing moment is real, but it is not inevitable, and it is not uniform. The sectors where India has genuine competitive advantages — pharmaceuticals, software services embedded in manufacturing, cost-competitive labour-intensive assembly — are growing. The sectors where India aspires to compete — semiconductor fabrication, precision automotive components, advanced electronics — face structural constraints that require sustained, multi-decade investment to address.

For businesses making capital allocation decisions, the framework should be sector-specific rather than country-level. ‘Manufacturing in India’ is not a single proposition; it is 30 different propositions depending on the product, the location within India, the customer geography, and the time horizon of the investment. The businesses that will capture India’s manufacturing opportunity are those that engage with that specificity — that do the granular analysis of power supply at the specific industrial park, the skills availability in the specific catchment area, the logistics cost for the specific product to the specific customer market — rather than relying on the headline narrative.

The headline narrative is bullish. The granular analysis, for many specific manufacturing decisions, is more nuanced. Both things are true, and holding both simultaneously is what sound investment strategy in India’s manufacturing sector requires.