The US healthcare system’s fee-for-service business model has been recognised as economically dysfunctional for at least three decades. Under fee-for-service, healthcare providers earn revenue by providing more services — more office visits, more procedures, more diagnostic tests, more hospital admissions. The incentive structure produces predictable results: rising healthcare spending, uneven quality, and outcomes that fail to justify the aggregate cost. American healthcare spending has approached 18% of GDP, roughly double the OECD average, while producing health outcomes that trail most peer nations on almost every measurable dimension.

Value-based care emerged as the alternative business model in the mid-2000s and became the central policy direction of the Affordable Care Act of 2010. The concept is straightforward: payment structures that reward providers for producing better patient outcomes rather than more services. The implementation has been substantially slower than early advocates hoped, hampered by data infrastructure gaps, contentious negotiations between payers and providers over risk allocation, and the operational complexity of measuring outcomes across fragmented care delivery. But the trajectory has now shifted decisively. Value-based arrangements are no longer marginal experiments — they are the operational business model for a growing majority of Medicare beneficiaries and an expanding portion of commercial health insurance.

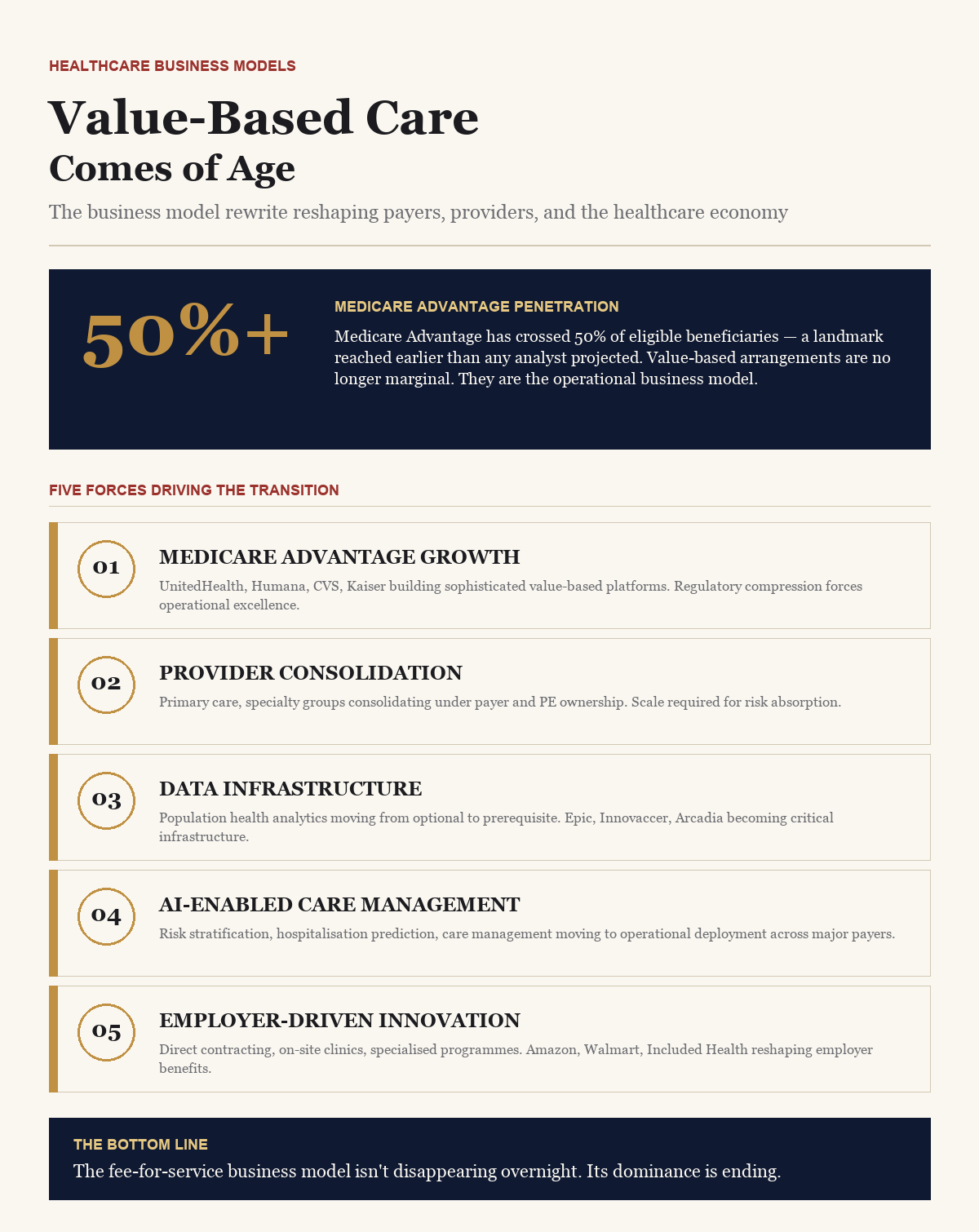

Medicare Advantage as the Growth Engine

The most significant driver of value-based care adoption has been the rapid growth of Medicare Advantage, the private health insurance alternative to traditional Medicare. Medicare Advantage enrolment crossed 32 million beneficiaries in 2024 and passed 50% of total Medicare-eligible population — a landmark that had been projected for decades but reached earlier than most analysts expected. The economics of Medicare Advantage plans force value-based operating models: plans receive a fixed per-member payment from the federal government and must manage total healthcare costs within that payment, which rewards effective preventive care, chronic disease management, and coordinated care delivery.

The dominant Medicare Advantage players — UnitedHealthcare, Humana, Aetna (CVS Health), Anthem, and Kaiser Permanente — have built increasingly sophisticated value-based care operating capabilities. UnitedHealth Group’s Optum division, which combines healthcare delivery, data analytics, and pharmacy benefits, has become the most visible model of vertically integrated value-based care. Humana has consolidated its focus on Medicare and value-based care to become effectively a Medicare-focused enterprise. CVS Health’s acquisition of Signify Health and Oak Street Health expanded its capacity to deliver primary care at scale within value-based frameworks.

The regulatory environment for Medicare Advantage has become more challenging in the past two years. The Centers for Medicare and Medicaid Services has tightened risk adjustment methodologies, cracked down on aggressive coding practices that had inflated Medicare Advantage revenue, and adjusted the annual payment rate updates in ways that have compressed margins for major players. The response from major Medicare Advantage insurers has been to double down on operational excellence in value-based care delivery — since the payment environment no longer supports aggressive revenue extraction, cost management through effective care becomes the primary path to profitability.

Provider Consolidation Follows the Payment Model

Healthcare provider organisations have been consolidating rapidly, and the consolidation pattern follows the payment model incentives. Health systems that succeed in value-based arrangements need scale to absorb risk, sophisticated data infrastructure to manage populations, and comprehensive care delivery capabilities across primary care, specialty care, hospital care, and post-acute care. This has produced a consolidation wave among health systems, primary care groups, and specialty practices.

The primary care segment has seen particularly aggressive consolidation. Oak Street Health (acquired by CVS), One Medical (acquired by Amazon), Iora Health (acquired by One Medical), and dozens of smaller value-based primary care organisations have been consolidated by larger payers and delivery organisations. The business model of these value-based primary care groups is fundamentally different from traditional primary care: they receive per-patient capitation payments and are responsible for total healthcare cost management, which changes the operational model from volume-based visits to comprehensive population health management.

Specialty care organisations are following a similar consolidation pattern but with more variation. Dermatology, ophthalmology, gastroenterology, and orthopedics have all seen substantial private equity-backed consolidation as investors have identified the potential for value-based specialty contracting. The economics of these deals often depend on the ability to transition from purely fee-for-service revenue to shared-savings or bundled payment arrangements that reward efficiency and outcomes. The consolidated organisations have the scale and infrastructure to negotiate and manage these arrangements in ways that independent specialty practices typically cannot.

The Data Infrastructure That Value-Based Care Requires

Effective value-based care operations require data infrastructure that most healthcare organisations have not historically built. Population health management requires visibility into which members have chronic conditions, which are at risk of costly hospitalisations, which have gaps in evidence-based care, and which providers are producing the best outcomes at the lowest cost. Building this visibility requires integrating claims data, electronic health record data, patient-reported outcomes, and specialised registries in ways that most healthcare organisations struggle to do.

The data infrastructure investments have been substantial. Major payers spend hundreds of millions of dollars annually on population health analytics platforms, care management systems, and provider network performance measurement. Delivery organisations moving into value-based care require comparable investments to succeed. The vendors serving this need — Epic Systems, Cerner (now Oracle Health), Innovaccer, Arcadia Analytics, and a proliferation of specialised analytics companies — have become critical infrastructure providers to the value-based care ecosystem.

Artificial intelligence has emerged as a critical enabling technology for value-based care operations. Machine learning models for identifying high-risk members, predicting hospitalisation risk, optimising care management interventions, and detecting fraud and waste have moved from experimental to operational deployment across major payer and provider organisations. The competitive advantage from AI-enabled population health management is measurable and growing, and organisations without credible AI capabilities in this domain face structural disadvantage.

Employer-Sponsored Insurance Follows Medicare’s Lead

Commercial employer-sponsored health insurance, which covers approximately 155 million Americans, has been slower to embrace value-based care than Medicare Advantage but is now moving in that direction more aggressively. Large employers have grown frustrated with double-digit annual healthcare cost increases and are actively pursuing alternative approaches. Direct contracting with high-quality health systems, on-site or near-site clinics, reference-based pricing arrangements, and specialised value-based programmes for specific conditions have all seen substantial commercial adoption.

Amazon’s approach to employee healthcare, including its acquisition of One Medical and various on-site clinic arrangements, has been influential in shaping employer thinking about value-based care. Walmart’s healthcare delivery expansion (though partially pulled back in 2024) and CVS Health’s HealthHUB initiatives have similarly demonstrated that non-traditional players are willing to build value-based care delivery capabilities directly rather than working through existing intermediaries.

The employer-focused value-based care startups — Included Health, Transcarent, Nomi Health, Firefly Health, and numerous others — have raised substantial capital to build alternatives to traditional health insurance and provider arrangements. The commercial economics have been challenging, and several of the earliest-generation companies have contracted or exited the market. But the underlying employer demand for effective healthcare cost management remains strong, and the companies that develop scalable models will find substantial commercial opportunity.

The Challenges That Persist

Value-based care has not resolved all of the healthcare system’s structural challenges. Provider adoption remains uneven, with many independent practices and specialty groups continuing to operate primarily under fee-for-service arrangements. The measurement infrastructure for quality and outcomes remains imperfect, with contested methodologies for risk adjustment and outcome attribution. The financial incentives for providers to succeed in value-based care are still weaker in many arrangements than the financial incentives to maximise fee-for-service revenue.

Rural healthcare markets have proven particularly difficult for value-based care implementation. The population densities and provider capacity in rural areas often do not support the operational infrastructure that value-based care requires. Federal programmes have attempted to address rural value-based care through specialised payment models and technical assistance, with modest results. The rural healthcare access gap between value-based care outcomes in dense metropolitan markets and rural markets has widened rather than narrowed over the past decade.

Medicaid populations present their own set of value-based care implementation challenges. Medicaid managed care organisations serve populations with more complex social needs, greater instability in coverage, and less continuity of care than commercial or Medicare populations. Effective value-based care for Medicaid populations requires social service integration, community-based interventions, and long-term relationship building that traditional managed care operations often struggle to provide effectively.

What the Next Five Years Will Look Like

The trajectory for the next five years is toward continued expansion of value-based care as the operational business model for a majority of American healthcare. Medicare Advantage penetration is projected to reach 60% by 2028. Employer-sponsored commercial insurance is likely to see continued erosion of pure fee-for-service arrangements. Medicaid managed care will continue to evolve toward more sophisticated value-based frameworks.

The organisations that succeed in this environment will share several characteristics. They will have integrated care delivery capabilities that span the continuum from primary care through specialty care to post-acute care. They will have data and analytics infrastructure that supports genuine population health management. They will have compensation and incentive structures that align individual provider behaviour with organisational value-based care performance. And they will have cultures that treat outcomes and total cost of care as the primary metrics of organisational success rather than as secondary considerations.

For healthcare executives, the strategic implications are significant. The traditional fee-for-service business model is not disappearing overnight, but its dominance is ending. Organisations that continue to operate primarily under fee-for-service assumptions while the market shifts to value-based frameworks will face declining competitive position. Organisations that invest in the capabilities required for value-based care success — care management infrastructure, data analytics, population health management, provider network performance measurement — will be positioned to lead the industry through its most significant business model transition in generations. The rewrite is happening. Whether individual healthcare organisations are prepared for it is now a strategic decision, not an operational abstraction.