The confrontation between the United States, Israel, and Iran has been the most consequential geopolitical development of 2026. What began as escalating regional tensions in early 2025 has hardened into a sustained conflict pattern involving direct military exchanges between Israel and Iran, expanded US sanctions on Iranian oil exports, Iranian-backed proxy attacks against shipping in the Persian Gulf and Red Sea, and the most militarised state of the Strait of Hormuz since the 1980s tanker war. The economic consequences of this conflict have moved well beyond the political sphere into the operational reality of businesses across almost every industry that depends on energy inputs, shipping routes, or supply chains that touch the Middle East.

For business leaders reading the daily headlines about missile exchanges, sanctions announcements, and Iranian retaliation threats, the challenge is to translate the geopolitical noise into concrete operational implications. This article sets out what the conflict has already done to energy markets, what the credible near-term scenarios look like, and what specific actions business leaders should be taking to manage the exposures that this new energy order creates.

What Has Already Changed in Energy Markets

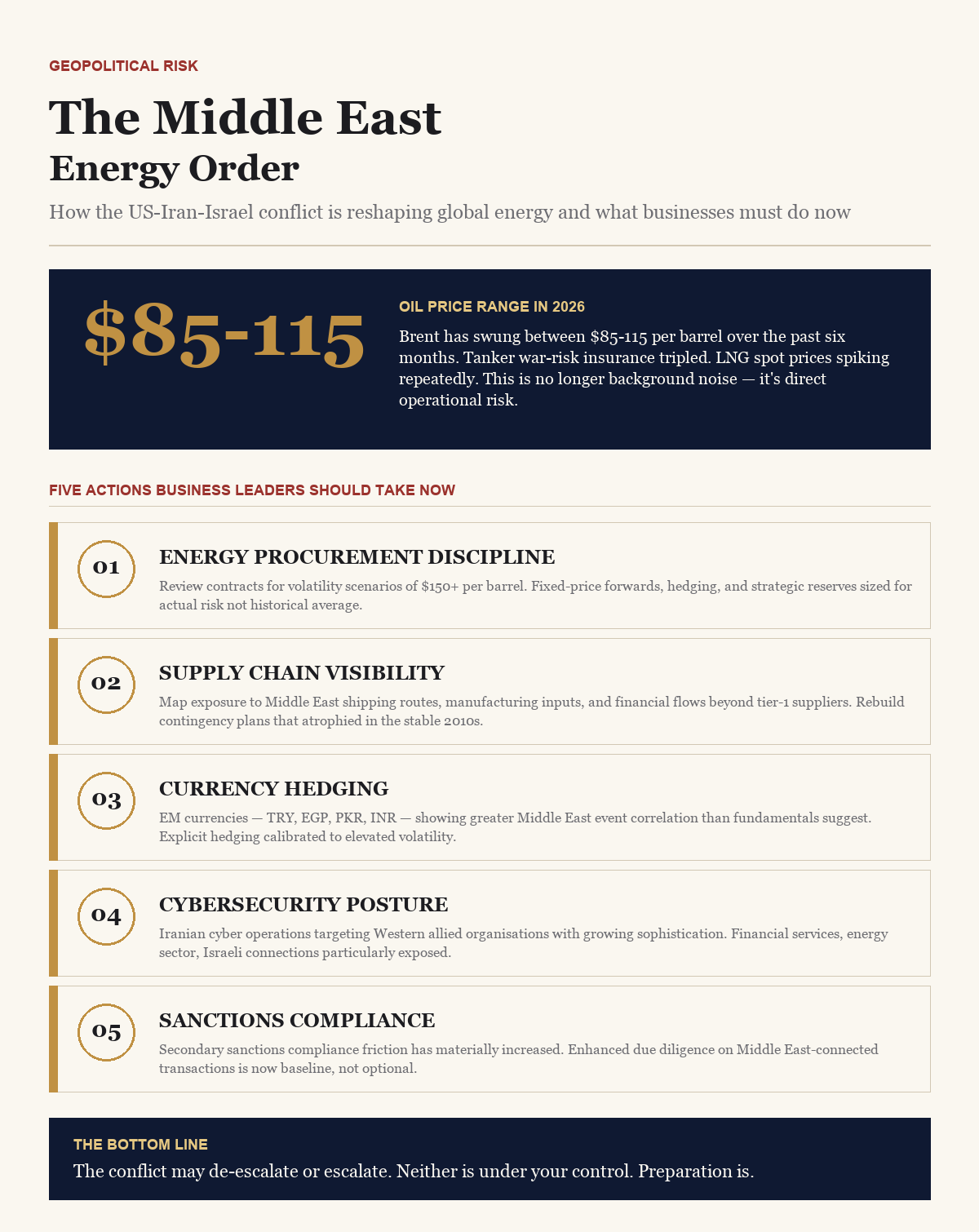

Oil prices have been the most visible manifestation of the conflict’s economic footprint. Brent crude has traded in a $85 to $115 range for most of 2026, with sharp spikes coinciding with direct military exchanges or escalation announcements. The volatility itself, independent of the average price level, has been the more consequential factor for corporate finance planning. When oil prices can move $15 per barrel over 48 hours in response to a missile exchange, procurement and hedging decisions become substantially more difficult, and the cost of carry on inventory increases materially.

Liquefied natural gas markets have been affected more asymmetrically than oil markets. Qatar’s LNG exports, which represent approximately 20% of global LNG supply, transit through the Strait of Hormuz. Each escalation cycle has produced spot LNG price spikes in Europe and Asia that far exceed the corresponding oil price moves. European gas storage strategies, Japanese and Korean utility procurement practices, and Indian LNG import pricing have all been forced to adapt to the possibility of sustained Qatar LNG disruption in ways that were not seriously contemplated even three years ago.

Shipping and insurance costs have adjusted dramatically. War risk insurance premiums for vessels transiting the Strait of Hormuz have tripled since early 2025. The Suez Canal-Red Sea route, which had been partially reopened in 2024 following Houthi attacks on shipping, faced renewed disruption in 2026 as Iranian-backed proxies expanded targeting to include tankers with any US, UK, or Israeli commercial connection. The alternative routing around the Cape of Good Hope adds approximately three weeks to shipping timelines and materially increases fuel costs. Supply chains that assumed reliable Middle East shipping infrastructure have been forced to rebuild contingency plans that many organisations had allowed to atrophy during the more stable 2010s.

The Sanctions Escalation and Its Complications

The United States has substantially expanded sanctions against Iranian oil exports over the past 18 months. Secondary sanctions now apply to any financial institution facilitating Iranian oil purchases and to shipping companies moving Iranian oil, regardless of jurisdiction. The enforcement has been more active than in previous sanctions cycles, with substantial penalties levied against Chinese financial institutions and several dozen shipping companies added to Treasury Department designated lists in 2026 alone.

The complications of this sanctions expansion extend beyond direct Iranian oil trade. Chinese refineries that had been the primary buyers of Iranian oil have been forced to restructure their crude sourcing, which has affected pricing across the Asian sour crude market. Indian refineries, which have historically maintained sanctions-compliant relationships with Iran while purchasing modest volumes, have faced increased compliance pressure. Global oil trading firms have become more cautious about intermediating Middle East oil transactions, adding operational friction to legitimate trade.

For businesses with any exposure to Middle East supply chains — even businesses whose direct products or services have nothing to do with oil — the sanctions environment has become substantially more complex. Financial institution reviews of Middle East-connected transactions have intensified. Legal and compliance costs for international operations touching the region have risen. The operational overhead of doing business in and through the Middle East has increased in ways that were not visible five years ago but are now a routine cost of international commerce.

The Scenarios That Businesses Must Plan For

The credible scenarios for the next 12 to 24 months of the conflict range from measured de-escalation to substantial regional war, and business planning needs to accommodate the full distribution rather than assuming any particular outcome. Four scenarios warrant explicit planning attention.

The first scenario is sustained tension without major military escalation — essentially a continuation of the current pattern of intermittent exchanges, sanctions pressure, and shipping disruptions. Under this scenario, oil prices continue to trade in a wide range with periodic spikes, shipping and insurance costs remain elevated, and the operational overhead of Middle East-connected commerce continues. This is arguably the highest-probability scenario for the next 12 months, and it is the environment for which most business planning should be primarily calibrated.

The second scenario involves partial resolution through diplomatic engagement — a negotiated pause or framework agreement that reduces immediate escalation risk without resolving the underlying tensions. Under this scenario, oil prices would decline moderately, shipping costs would normalise partially, and business operational overhead would ease. Historical precedents suggest that the resulting relative stability would likely be temporary, but even six to twelve months of reduced tension would allow businesses to recover from the accumulated stress of 2025-2026.

The third scenario is significant escalation short of full regional war — perhaps direct US military action against Iranian nuclear or military infrastructure, followed by Iranian retaliation against regional US assets and shipping. Under this scenario, oil prices would spike sharply, likely into the $150 to $200 per barrel range, with substantial impact on inflation, growth, and financial market stability globally. Businesses planning for this scenario need explicit contingency plans for sustained supply chain disruption, extreme energy cost volatility, and potentially significant currency movements.

The fourth scenario is full regional war involving direct conflict between US and Iranian military forces, potential closure of the Strait of Hormuz, and possible expansion to include other regional actors. This scenario is low-probability but not zero, and its consequences would be severe enough that even a low probability warrants some level of contingency planning. Oil prices could exceed $200 per barrel, global growth could enter recession, and specific supply chains could face disruptions measured in months rather than weeks.

What Business Leaders Should Actually Do

The practical actions that business leaders should be taking to manage exposure to the US-Iran-Israel conflict fall into several categories that vary in urgency and implementation timeline. The most immediate priorities involve current operational exposures; longer-term priorities involve strategic positioning for a sustained period of Middle East volatility.

Energy procurement discipline has become substantially more important than it was in stable periods. Businesses with material energy costs — manufacturers, logistics operators, energy-intensive industrial producers, hospitality companies with large facility portfolios — should be reviewing their energy procurement contracts with explicit attention to the price volatility scenarios described above. Fixed-price forward contracts, hedging programmes, and strategic reserves should be sized appropriately for the risk environment rather than the historical average. Companies that assumed forward energy costs based on 2019-2021 pricing patterns are systematically underprepared for the current environment.

Supply chain visibility must extend beyond first-tier suppliers to include the routing, insurance, and financial infrastructure that supports supply chain execution. Businesses that have not mapped their supply chain exposure to Middle East shipping routes, Middle East manufacturing inputs, or Middle East-connected financial flows may be surprised by second-order disruptions during escalation events. The mapping exercise is not particularly expensive but requires deliberate effort that many organisations have deferred.

Currency and financial hedging strategies need to reflect the increased correlation between Middle East geopolitical events and global financial markets. Emerging market currencies, particularly in Turkey, Egypt, Pakistan, and India, have shown greater volatility during Middle East escalation cycles than the fundamentals would suggest. Businesses with significant exposures to these currencies should have explicit hedging strategies calibrated to elevated volatility rather than historical norms.

Cybersecurity attention to Iranian-linked actors has grown warranted. Iranian cyber operations, both directly state-sponsored and through proxy groups, have targeted Israeli, American, and Western allied organisations with increasing sophistication. Financial services firms, energy sector companies, and organisations with any Israeli connections have been particularly targeted. Cybersecurity teams should be actively engaged with intelligence about Iranian threat actor activity and should be prepared for both destructive attacks and prolonged espionage campaigns.

The India Dimension

For Indian businesses, the US-Iran-Israel conflict presents specific complications that reflect India’s unique diplomatic and commercial position. India has maintained working relationships with the United States, Israel, and Iran simultaneously — a diplomatic balance that has become substantially more difficult to sustain as the confrontation has intensified. Indian oil imports from Iran, though reduced significantly since the resumption of US sanctions, remain a source of ongoing diplomatic tension with Washington. Indian defence and technology cooperation with Israel has expanded even as Indian participation in Iranian projects has been curtailed.

For Indian companies with international operations, the compliance environment has become more demanding. Financial transactions with Iranian counterparties require heightened due diligence to avoid inadvertent violation of US secondary sanctions. Shipping and logistics operations with Middle East exposure require enhanced war risk insurance and routing flexibility. Currency hedging for Indian rupee exposure has become more important as INR volatility has increased during Middle East escalation cycles.

India’s energy security position remains fundamentally exposed to Middle East disruption. Approximately 60% of India’s crude oil imports and 40% of LNG imports transit through the Strait of Hormuz. The strategic petroleum reserves, expansion of Russian and US crude sourcing, and pipeline diversification through the Chabahar port in Iran and Central Asian connections have all been priorities but remain partial solutions. Indian businesses should assume that Indian energy costs will remain elevated and volatile for the foreseeable future, and should build that assumption into their financial planning.

The Long-Term Structural Implications

Beyond the immediate operational implications, the US-Iran-Israel conflict is accelerating several structural shifts in the global energy and business landscape that will define the coming decade. The most consequential is the acceleration of energy diversification investment away from Middle East dependence. European gas storage expansion, Japanese and Korean LNG contracting flexibility, US LNG export capacity expansion, and Indian renewable energy investment have all accelerated in response to Middle East supply uncertainty. The physical and financial infrastructure being built now will outlast the current conflict and will structurally reduce Middle East strategic leverage over the coming decade.

The renewable energy transition has received an additional accelerant from Middle East instability. Every escalation cycle produces political and commercial support for renewable energy investment that would be harder to justify in a stable oil price environment. Solar and battery deployment in emerging markets, particularly India and sub-Saharan Africa, has been supported by the economic case that fossil energy prices are structurally uncertain in ways that make renewable investment more attractive on a risk-adjusted basis than the levelised cost comparison alone would suggest.

Regional realignment continues to reshape the international system’s response to Middle East instability. The expansion of the BRICS grouping to include Saudi Arabia, the UAE, and Iran has created a diplomatic framework in which Middle Eastern conflicts play out with different actors and different mediation dynamics than the pre-2020 US-dominated international order provided. The consequences of this realignment for business operations are complex, but the general direction is toward greater multipolarity and reduced predictability of international responses to crises.

The Bottom Line

The US-Iran-Israel conflict is not a distant geopolitical story with peripheral business implications. It is a direct operational risk factor affecting energy costs, supply chain reliability, financial market volatility, cybersecurity exposure, and international regulatory complexity for businesses across almost every industry. The organisations that manage this risk well will be those that treat it as a strategic priority requiring board attention, dedicated resources, and explicit contingency planning rather than as background noise to be managed reactively.

The conflict may de-escalate over the coming months, or it may escalate substantially. Neither outcome is under the control of business leaders. What is under their control is the quality of preparation their organisations bring to the range of scenarios that could unfold. The businesses that emerge strongest from this period of Middle East volatility will be those that made deliberate strategic choices about energy procurement, supply chain resilience, financial hedging, and operational contingency planning while the volatility was ongoing — rather than waiting for the situation to resolve before adapting to it.